New launches in Mumbai residential market increased by 33% in Q2 2021: JLL

New launches in Mumbai residential market increased by 33% in Q2 2021: JLL

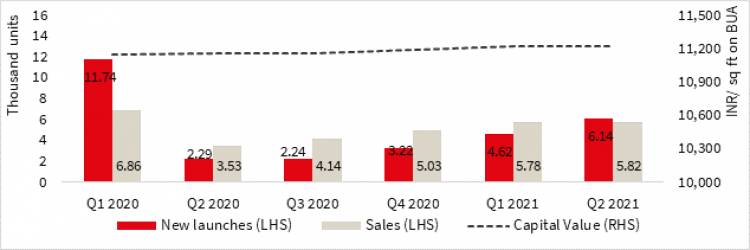

Mumbai, 26 July, 2021: New launches in the Mumbai residential market increased by 33%, from 4,616 units in Q1 2021 to 6,143 units in Q2 2021, as per a recent study by JLL. While sales in the city remained at similar levels of Q1 2021, transactions were concentrated in the price segment of INR 50 lakh to INR 1 crore, which accounted for 40% of the sales during the quarter.

Eastern suburbs accounted for the majority of new launches with 25%, followed by Western suburbs II (comprising of Malad, Kandivali, Borivali and Dahisar) with 22%. In terms of sales, Thane and Navi Mumbai combined reported close to 50% of sales. When compared to Q1 2021 capital value of residential units in the city remained stable in Q2 2021.

Mumbai – trends in launches & sales

Mumbai includes Mumbai city, Mumbai suburbs, Thane city and Navi Mumbai

Source: Real Estate Intelligence Service (REIS), JLL Research

Further, most of the new launches in Mumbai were in the affordable and mid segment (ticket size upto INR 2 crore) and formed 84% of the launches during the quarter. In sync with demand, developers are expected to focus on these price segments.

Karan Singh Sodi, Regional Managing Director, JLL India said, “The increase in sales presents clear signs of demand and buyer confidence coming back to the market. This has been on the back of historically low home loan interest rates, stagnant residential prices, lucrative payment plans and freebies from developers and government incentives such as the reduction of stamp duty.”

Mumbai has consistently been the largest contributor to sales over the past five quarters and the trend continued in Q2 2021 as well. Almost one-third of the sales volume was contributed by the city during the quarter.

Residential sales across the top seven cities in Q2 (April-June) 2021 increased by 83% as compared to Q2 2020, across the top seven cities. According to JLL’s Residential Market Update – Q2 2021 released recently, this was mainly due to low base effect, less stringent lockdowns, and accelerating vaccination drives during Q2 2021, demonstrating improved resilience in the market. During the first wave of COVID-19, residential sales dropped by a record 61% quarter-on-quarter to 10,753 units in Q2 2020. However, the impact of the second wave has been limited with sales in Q2 2021 dipping by 23% to 19,635 units.

Dr. Samantak Das, Chief Economist and Head Research & REIS, India, JLL said “The residential sector displayed improved resilience in Q2 2021 when compared to Q2 2020. There is no denying the fact that the second COVID-19 wave dented the market following a good recovery curve. However, the impact was muted when compared to the same period last year. Most of the changes observed in the sector have been structural in nature and demand for homes is only expected to increase. The RBI is expected to hold policy rates at the existing historically low levels, while prices will remain mostly range bound. The resultant affordable buoyancy will continue to attract fence sitters and serious homebuyers,”.

“If the downward trajectory in COVID-19 cases is sustained, the sector is expected to make a healthy recovery in the second half of 2021,” he added.

Established developers will continue to run the show

Structural reforms within real estate in the last few years started the process of weeding out smaller, unorganised developers from the market. The COVID-19 pandemic tilted the scale further in favour of established developers. Homebuyers have also become even more cautious in affecting their home purchase decisions. There is an increased preference and willingness to pay a premium for projects by developers with an established track record.

New launches expected to go up in H2 2021

On average, new launches of more than 35,000 units were witnessed every quarter between Q1 2019 and Q1 2020. In the COVID-era (Q2 2020 – Q2 2021), this has decreased to ~23,000 units.

Sustained growth of the sector in the second half of 2021

There is no denying the fact that the second COVID-19 wave dented the market following a good recovery curve. However, the impact was muted when compared to the same period last year. Most of the changes witnessed in the sector have been structural in nature and demand for homes is only expected to increase. Importantly, lockdown restrictions across cities are being eased and the vaccination drive is gathering pace. If the downward trajectory in COVID-19 cases is sustained, the sector is expected to make a healthy recovery in H2 2021.